Low-cost ULIPs have recently entered the market (2005) and brought in stiff competition for Mutual funds.

Low-cost ULIPs have recently entered the market (2005) and brought in stiff competition for Mutual funds.

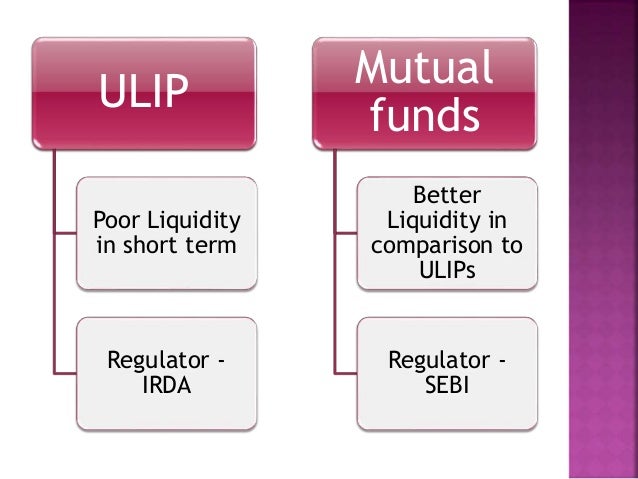

Between ULIPs and MFs, it is not about which one is better and where to invest. Rather your deciding factor should be what do you want and who you are. Understand your requirements - Do you want to invest or buy insurance or both? Do you want garanteed returns (or) are you fine with some risk?

Parameters |

ULIP |

Mutual Fund |

Definition

|

ULIP allow investors to direct part of their premiums into different types of funds (Equity, Growth, Money market, SBI Bond, etc.). |

A mutual fund pools the money from investors and uses it to invest in various securities according to a pre-specified investment objective. |

Purpose

|

For both Investment and Insurance purpose.

|

Primarily for Investment purpose. No Insurance benefit.

|

Lock-in-Period

|

Lock in period for 5 years; you can withdraw your money.

If the policy is discontinued in the first year, the surrender charge is 20%

of the premium.

|

There is no Entry load and after one year there is no Exit

load either. You can enter and exit at any time depending on market

conditions and personal choice.

|

Loyalty Benefits

|

It comes with long-term investment.

|

No Loyalty (or) Long-term Investment benefits.

|

Track Record

|

Actually came into existence from 2005.

|

Established Product. Until 1987, UTI enjoyed monopoly in

market, and then host of government financial companies came up with their

own funds.

|

Tax Status

|

All Unit Linked

Plans offer tax benefits under section 80C.

|

Only investments in tax

saving funds are eligible for section 80C benefits.

|

Charges Structure

|

Charges in a unit

linked plan include mortality charges for the life insurance provided. In

addition, premium allocation charge, fund management charge and

administration charges are applicable.

|

Mutual fund charges

include an entry load, the annual fund management charge and an exit load, if

applicable.

|

{kind=link}