Equity markets have delivered 15.9%* compounded annual returns in the last 15 years. Investments in good companies held for long term has helped in savings and creation of wealth for retail investors.

Benefits of Equity SIP (SEP):

Start investment with small amount

Rupee cost averaging

Diversification

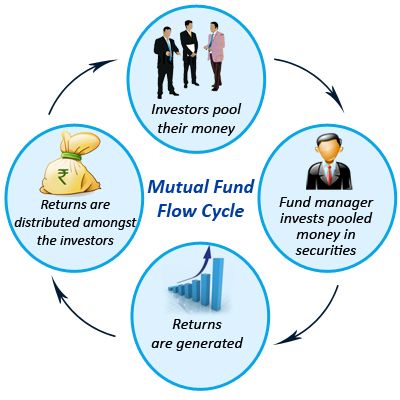

Nifty ETF- Retail Investors have option to start investing directly in top companies in India or buy Nifty which is an index of top 50 companies in India basis market capitalization through an Exchange traded Fund (ETF).

Up-to Free Brokerage of Rs 1000 for your account, if you start doing systematic Investments in ETFs:

1. Rs.500 as free brokerage will be credited to your account if you start investing within 7 days of account opening. If you only login but do not trade within 7 days of account opening then you will get Rs 250 as free brokerage.

2. Additional Rs.500 as free brokerage will be credited in your account if you start a Systematic Equity Plan in ETFs within subsequent 1 month of account opening i.e. T+1 month of account opening where T is the month of account opening.

Terms & Conditions for free brokerage:

Free brokerage cannot be liquidated or claimed for refund

ICICI group employees are not eligible for free brokerage offer

Validity for free brokerage will be 6 months from account opening

Free brokerage would be credited on next working day of 1st Login, 1st Trade and SEP request date.

*Period of Stock Market (NSE) returns (CAGR) is from June 07, 2002 to June 06, 2017.

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------Customer Acknowledgement:

Please find details of your Systematic Investments

Monthly Investment value (Rs)

Total Months (SIP Period)

ETF Code

Monthly investment amount or period can vary as per your choice

Maximum Monthly Investment value to be Rs.2500

Quantity of ETF credited to your demat account will be in whole numbers & decided as per the market price & Monthly investment value & not exceeding monthly investment value amount

For accounts opened from 1st of the current month to 20th of the current month, the SEP order will be placed in customers account on the next day of account opening date and if it is a holiday then SEP order will be placed on next working day. SEP shall trigger on T+2 day after SEP order placement.

For accounts opened from 21st of the current month to 31st of the current month, the SEP order will be placed in customers account on 1st of next month and if it is a holiday then SEP order will be placed on next working day.

Start your Systematic Investments now:

Please define details of your Systematic Investments

Monthly Investment value (Rs)

Total Months (SEP Period)

ETF Code/Name

For example : Rs.2000

For example : 24 month

ICINIF

ICICI Prudential Nifty ETF

Monthly investment amount or period can vary as per your choice.

Maximum Monthly Investment value to be Rs.2500 & maximum SEP period to be 24 months.

Quantity of ETF credited to your demat account will be in whole numbers & decided as per the market price & Monthly investment value & not exceeding monthly investment value amount.

For accounts opened from 1st of the current month to 20th of the current month, the SEP order will be placed in customers account on the next day of account opening date and if it is a holiday then SEP order will be placed on next working day. SEP shall trigger on T+2 day after SEP order placement.

For accounts opened from 21st of the current month to 31st of the current month, the SEP order will be placed in customers account on 1st of next month and if it is a holiday then SEP order will be placed on next working day

This is an SIP/SEP form which will debit your bank account every month for the above amount mentioned.

(Please tick box) I am aware & have understood the scheme/offer & want to start SEP as per above details.

Objective/purpose of investing: _________________________________________________________

Customer Signature: ________________________________

Version